What is the Rice Flour Market Overview – definition, scope, and significance?

Rice flour is a finely milled powder obtained from either white or brown rice grains. It serves as a gluten‑free alternative to wheat flour and is used in a wide range of food and beverage applications, including bakery, confectionery, snacks, baby foods, and breakfast cereals. The market’s scope extends across both organic and conventional categories, reflecting growing consumer demand for clean‑label and health‑focused ingredients. Significance lies in its role as a staple ingredient for gluten‑intolerant populations, its functional properties such as moisture retention and texture enhancement, and its contribution to the diversification of product portfolios for food manufacturers worldwide.

What are the key drivers, restraints, challenges, and opportunities in the Rice Flour Market?

Drivers include rising gluten‑free and clean‑label trends, increasing prevalence of celiac disease, and expanding middle‑class consumption in emerging economies. The shift toward organic products further fuels demand for organic rice flour. Restraints stem from price sensitivity compared with wheat flour and the requirement for specialized processing equipment. Challenges involve maintaining consistent quality across white and brown rice flour and addressing supply‑chain volatility for raw rice. Opportunities arise from product innovation— such as pre‑gelatinized rice flour for instant mixes— and from geographic expansion into regions where rice is a dietary staple, enabling manufacturers to capture new consumer segments.

What are the current growth trends shaping the Rice Flour Market?

Current trends feature a surge in “free‑from” product launches, particularly in the bakery and snack sectors, where rice flour is used to create crisp textures without gluten. Another trend is the incorporation of rice flour into plant‑based protein formulations, enhancing nutritional profiles. Sustainable sourcing is gaining prominence, with many brands highlighting responsibly grown rice. Finally, the rise of e‑commerce has accelerated the availability of niche rice flour varieties, such as organic brown rice flour, directly to consumers.

How did COVID‑19 impact the Rice Flour Market and what is the recovery trajectory?

The pandemic caused an initial demand dip due to disruptions in foodservice channels, but retail sales of gluten‑free and health‑oriented products surged as consumers cooked more at home. Supply‑chain bottlenecks in raw rice shipments were gradually resolved, and by late 2021 the market entered a recovery phase. The post‑COVID landscape shows a stronger focus on shelf‑stable, ready‑to‑use rice flour blends, supporting sustained growth through 2025 and beyond.

What does the competitive landscape of the Rice Flour Market look like?

The market is moderately consolidated, with several multinational and regional players holding strong positions. Key competitors such as Archer‑Daniels‑Midland Co., Ingredion Inc., and Ebro Foods SA dominate the bulk supply segment, while niche firms like Bob’s Red Mill Natural Foods Inc. and Bay State Milling Co. focus on specialty organic and non‑GMO offerings. Recent years have seen strategic alliances and acquisitions aimed at expanding product lines and geographic reach, indicating a trend toward consolidation.

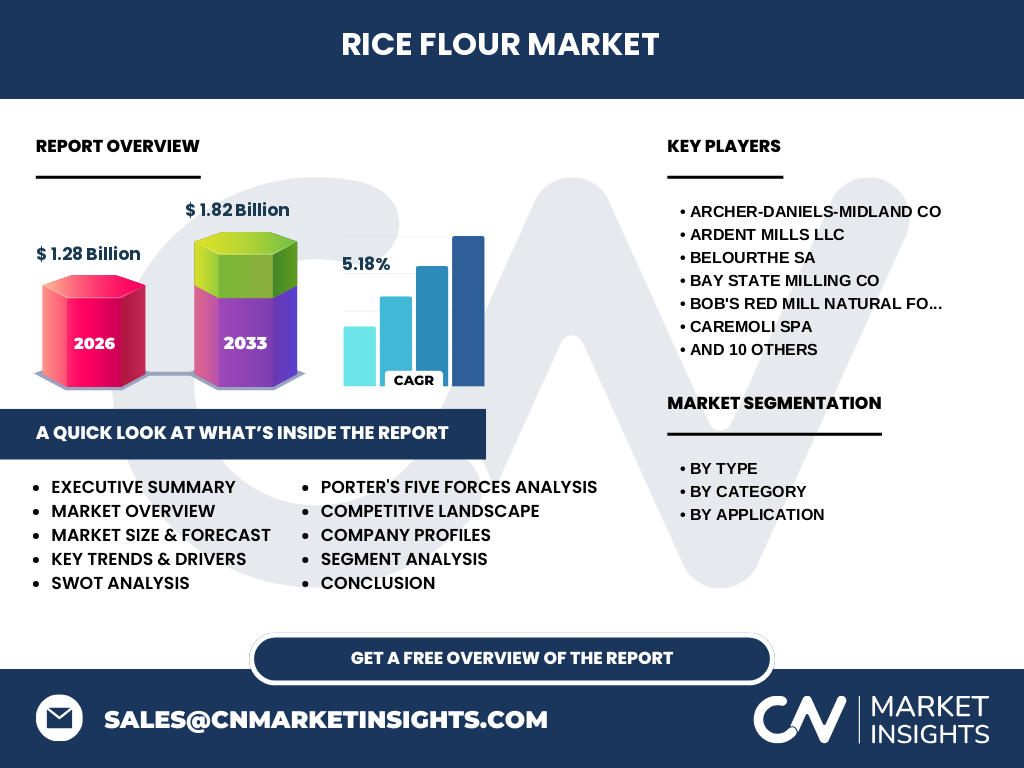

What are the high‑level findings in the Executive Summary of the Rice Flour Market?

The Rice Flour Market is valued at $1.28 billion in 2026 and is projected to reach $1.82 billion by 2033, reflecting a CAGR of 5.18 %. Growth is driven by gluten‑free trends, organic demand, and expanding applications across bakery, snacks, and beverages. White rice flour holds the larger share due to its neutral flavor, while brown rice flour gains ground for its nutritional appeal. Regional analysis highlights strong performance in Asia‑Pacific, with notable opportunities in North America and Europe for premium organic products. Competitive dynamics are marked by a blend of large multinational suppliers and agile specialty manufacturers.

What is the forecast for the Rice Flour Market from 2025 to 2032?

Based on the provided CAGR of 5.18 %, the market is expected to maintain steady growth through 2032. The forecasted valuation of $1.82 billion for 2033 suggests a continued upward trajectory, supported by expanding consumer awareness of gluten‑free diets and increasing adoption of rice flour in innovative food formats. Manufacturers are likely to invest in capacity expansion and product differentiation to capture incremental demand.

How is the Rice Flour Market sized and shared by segmentation?

By type, the market is divided into White Rice Flour and Brown Rice Flour. White rice flour commands a larger portion due to its versatility in neutral‑flavored applications, while Brown Rice Flour is prized for higher fiber and micronutrient content, appealing to health‑conscious segments. By category, Organic and Conventional segments differentiate on production practices; the organic niche, though smaller, is growing faster owing to premium pricing. By application, the market splits across Bakery & Confectionery, Beverages, Sweet & Savory Snacks, BaFood (baby foods), and Breakfast Cereals, each leveraging rice flour’s functional properties for texture, moisture, and nutritional enhancement.

What is the global Rice Flour Market size and share by region?

The global market is anchored by strong demand in Asia‑Pacific, where rice is a dietary staple and rice flour is integral to traditional cuisine. North America and Europe exhibit robust growth in the premium organic and gluten‑free segments. While exact regional monetary shares are not disclosed, the geographic distribution aligns with consumer preferences: high-volume conventional consumption in Asia‑Pacific and higher-value organic consumption in Western markets.

What are the key insights from the regional analysis of the Rice Flour Market?

Asia‑Pacific leads in absolute volume, driven by countries such as India, China, and Thailand, where rice flour is used in both traditional and modern snack products. In North America, the market is fueled by gluten‑free bakery items and health‑focused product launches, with organic rice flour gaining market share. Europe shows similar patterns, especially in Germany, the UK, and the Nordics, where regulatory support for clean‑label foods accelerates adoption. Latin America and the Middle East present emerging opportunities as consumer awareness of gluten‑free diets rises.

Which companies are leading in the Rice Flour Market and what are their strategies?

Archer‑Daniels‑Midland Co., Ingredion Inc., and Ebro Foods SA dominate bulk supply, focusing on scale, cost efficiency, and global distribution networks. Specialty players such as Bob’s Red Mill Natural Foods Inc. and Bay State Milling Co. emphasize organic certification, non‑GMO positioning, and direct consumer outreach. Recent strategic moves include product line extensions into pre‑gelatinized and fortified rice flour blends, partnerships with bakery manufacturers, and investments in sustainable sourcing to meet ESG expectations.

How does Porter’s Five Forces analysis apply to the Rice Flour Market?

Threat of new entrants is moderate; low entry barriers for small‑scale organic producers exist, but large‑scale operations require significant capital. Bargaining power of suppliers is relatively low, as raw rice is widely available, though quality variations can affect pricing. Bargaining power of buyers is moderate to high, especially in retail where numerous brands compete on price and label claims. Threat of substitutes includes other gluten‑free flours (e.g., almond, tapioca), which intensifies competition. Industry rivalry is strong, with both multinational giants and niche players vying for market share through innovation and brand differentiation.

What are the SWOT highlights for the Rice Flour Market?

Strengths: Gluten‑free status, versatile functionality, and alignment with health trends. Weaknesses: Higher cost relative to wheat flour and occasional supply inconsistencies. Opportunities: Expansion into organic and fortified product lines, penetration of emerging markets, and development of specialty blends for plant‑based foods. Threats: Competition from alternative gluten‑free flours and potential price volatility of raw rice due to climate impacts.

What does the value chain of the Rice Flour Market look like?

The value chain begins with rice cultivation and harvesting, followed by cleaning, milling, and sieving to produce white or brown rice flour. Next, the flour may undergo further processing such as enrichment, organic certification, or functional treatments (e.g., pre‑gelatinization). Distribution channels include bulk sales to food manufacturers, specialty packaging for retail, and e‑commerce platforms. End‑users span food processors, bakeries, snack producers, and direct‑to‑consumer retail.

What key investment insights can be drawn from the Rice Flour Market?

Investors should target companies with diversified product portfolios covering both conventional and organic segments, as the premium organic niche offers higher margins. Capacity expansion in regions with growing middle‑class populations (e.g., Southeast Asia) can capture volume growth. Partnerships with gluten‑free and plant‑based food brands present synergistic opportunities, while sustainability initiatives can enhance brand equity and meet regulatory expectations.

What conclusions can be drawn about the Rice Flour Market?

The Rice Flour Market is on a clear upward trajectory, underpinned by health‑driven consumer preferences and functional advantages in food manufacturing. While price sensitivity and supply challenges exist, the market’s resilience is evident through steady CAGR and expanding application areas. Companies that innovate with organic, fortified, and ready‑to‑use blends are positioned to capture the most significant share of future growth.

What research methodology was used to compile this report?

The study employed a blend of primary and secondary research. Primary data were gathered through interviews with industry experts, manufacturers, and key distributors. Secondary sources included company annual reports, trade publications, government databases, and reputable market research databases. Data triangulation ensured accuracy, while CAGR calculations were based on the provided market size figures (2026: $1.28 billion; 2033: $1.82 billion).

What is the scope of this research and its limitations?

The research covers the global Rice Flour Market, segmented by type, category, and application, and includes regional performance analysis. It focuses on market size, growth drivers, competitive dynamics, and forecasts up to 2033. Limitations arise from the reliance on publicly available data and the absence of granular regional revenue breakdowns, which may affect precise market‑share estimations.

Which key companies are highlighted and what recent developments have they announced?

Key companies include Archer‑Daniels‑Midland Co., Ardent Mills LLC, BELOURTHE SA, Bay State Milling Co., Bob’s Red Mill Natural Foods Inc., CAREMOLI SpA, Capitol Food Co., Ebro Foods SA, Gulf Pacific Rice Co Inc., Hometown Food Co., Ingredion Inc., Koda Farms Inc., Kroner‑Starke GmbH, Naturis SpA, PGP International Inc., and Western Foods LLC. Recent developments feature product launches of organic brown rice flour blends, strategic partnerships with gluten‑free bakery chains, acquisitions aimed at expanding capacity in Southeast Asia, and sustainability initiatives such as sourcing rice from certified responsible farms.